Congratulations On Your Independent, Alternative Media, You Disgruntled Consumers

This might not go the way you think it will go

Appearing on Joe Rogan last month, Marc Andreessen, the billionaire co-founder of Andreessen Horowitz, complained to Rogan there was this thing called the Consumer Financial Protection Bureau, and it was engaged in a nefarious scheme to “debank” Americans solely on the basis of their political opinions.

This is, in fact, a truly dystopian prospect. Imagine if, say, Chase or Bank of America could drop you as a client because you posted something someone there didn’t like about abortion or guns or Kamala Harris or whatever else. If the consumer finance system had this sort of power, the results would be catastrophic.

But this was a ridiculous claim on its face, given that the CFPB is specifically designed to protect consumers against rapacious companies against whom they have little recourse. And Andreessen couldn’t have been wronger about the CFPB’s stance on debanking if he had tried.

On Rogan’s program, Andreessen claimed the CFPB orders “debanking” — that is, forced shutting down of bank accounts and other financial tools — for those it believes have “the wrong politics.” But debanking is, for the most part, not a CFPB issue — and where it is, the CFPB is doing the exact opposite of what Andreessen claimed. In August, the CFPB filed a brief in a legal case arguing that debanking of religious conservatives is a form of discrimination. At a panel earlier this year, CFPB Director Rohit Chopra argued that this amounts to payment services’ “setting laws or conditions outside of the democratic process.” On Tuesday, the CFPB followed this up by making it clear a proposed new rule would, if finalized[,] stop the sale by data brokers of personal info to scammers, could also combat debanking that occurs because of identify [sic] theft or other fraud.

Andreessen’s claim never made sense. The point of the CFPB is to protect consumers against potentially rapacious financial institutions with far more power than them. Whatever you think of the Bureau, it’s very hard to imagine a situation in which it would team with financial institutions to help them kick off individual consumers. Hence the organization’s actual, anti-debanking stance.

So why did Andreessen spread these bizarre mistruths? Most likely because of a preexisting, business-related vendetta against the Bureau. Olen continues:

In 2021, the CFPB shut down a fintech named LendUp Loans after the agency flagged and fined it multiple times for offenses including lying to customers and tricking them into taking on high-interest loans. Earlier this year, the bureau announced it would distribute nearly $40 million to “118,101 consumers who were deceived by LendUp Loans.” It was a humiliating end for a firm whose backers, according to The Wall Street Journal, included “some of the biggest names in venture capital, including. . . Andreessen Horowitz.” Yes, that Andreessen.

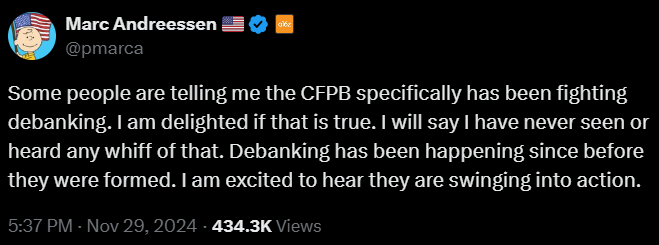

On Twitter, Andreessen eventually, kinda-sorta admitted to having been wrong: “Some people are telling me the CFPB specifically has been fighting debanking. I am delighted if that is true. I will say I have never seen or heard any whiff of that. Debanking has been happening since before they were formed. I am excited to hear they are swinging into action.”

The swing here was striking. On Rogan’s podcast, Andreessen was quite confident he knew enough about the CFPB to criticize it in no uncertain terms. Here’s that bit of the transcript, via an Andreessen-sympathetic Medium blogger:

Marc Andreessen: And then my favorite twist is we have this thing called independent federal agencies. So like for example, we have this thing called the Consumer Finance Protection Bureau [sic], CFPB, which is sort of Elizabeth Warren’s personal agency that she gets to control. And it’s an independent agency that gets to run and do whatever it wants, right? And if you read the Constitution, there is no such thing as independent agency, and yet there it is.

Joe Rogan: What does her agency do?

MA: Whatever she wants. Basically, terrorize financial institutions, prevent new competition, new start-ups that want to compete with the big banks.

JR: Really?

MA: Oh yeah, 100%.

JR: How so?

MA: Just terrorizing anybody who tries to do anything new in financial services.

JR: Can you give me an example?

MA: Oh, you know, debanking. This is where a lot of the debanking comes from, is these agencies. So debanking is when you as either a person or your company are literally kicked out of the banking system.

JR: Like they did to Kanye.

So on Joe Rogan, speaking to millions of people, Andreessen is confident enough in his knowledge of the CFPB to accuse it of debanking. Then, when people point out that what he’s said is wrong, he suddenly isn’t very familiar with the CFPB, its mission, and its stance on debanking (despite this being public information, and despite one of Andreessen’s companies having had a run-in with the Bureau). This tweet has more than a whiff of How should I know exactly what the deal is? I’m just a simple country tech billionaire. I know little of your “regulations” and “agencies.”

It’s exceptionally disingenuous, is what I’m saying.

Andreessen was aided in his attack on the CFPB by the fact that neither Joe Rogan nor his producer were in a position to push back. That’s one of the problems with Rogan’s show (which, full disclosure, I have been on). It has gotten very, very big, but Rogan is not a naturally skeptical person, so when someone comes onto his show with strong beliefs, an agenda, or both, he tends to get steamrolled by them. And it is hard to fact-check stuff like this in real time, especially if you don’t have any issue-area experts on hand, which Rogan never does. That’s why Rogan didn’t push back at all and accepted, at face value, Andreessen’s story about how the CFPB “terrorizes” people.

Keep reading with a 7-day free trial

Subscribe to Singal-Minded to keep reading this post and get 7 days of free access to the full post archives.